Which credit score is most accurate and why are they different?

Which credit score is most accurate and why are they different?

Working to improve your credit score can make you more attractive to lenders, but which credit score is most accurate? The truth is that they’re all accurate, in their own way. Read on to discover the differences between credit scoring models, then get LifeLock Total to monitor your credit and help protect against fraud.

A credit score is a number that represents your creditworthiness, or how likely lenders are to trust your ability to manage debt. Your credit score affects your chances of success when applying for a new credit card, loan, or mortgage. It’s even considered by some landlords or employers when assessing your financial responsibility.

There isn’t just one type of credit score; there are various credit scoring models that lenders use to evaluate your creditworthiness. Here’s everything you need to know about the different credit scores.

What is the most accurate credit score?

There’s no single most accurate or universally important credit score. Different scoring models use many of the same factors, such as payment history and credit utilization, but they weigh them differently and often use distinct scoring ranges. That’s why your score can vary by provider.

That said, FICO Score and VantageScore are the two most commonly used credit scores by lenders assessing loan approvals, credit cards, and mortgages. So, in that sense, you could consider them the most accurate indicators of how likely you are to be approved for a new credit application.

Why are my credit scores different?

Your scores are different because there are many models for calculating credit scores, and each uses a unique formula to evaluate your creditworthiness.

Here are some of the key variables that explain why your credit scores are different:

Credit bureaus: Most credit scores pull data from credit bureaus, but they don’t all necessarily use the same data from the same bureaus. That means they’re all working with different information, leading to variations in your scores.

Credit scoring models: Each credit scoring model uses different factors, and different weightings of those factors, to calculate a final score. There are even variations between different versions of specific models, which explains why your VantageScore 3.0 might differ from your VantageScore 4.0, for example.

Credit score type: Some credit scores offer different views that adjust the formula to suit specific use cases, like auto loan or mortgage applications. The specific criteria used in different credit score types result in different final scores.

Calculation date: Your credit score is constantly evolving as new information gets added to your credit history. As a result, even if you check your score using the same model, it can vary from one inquiry to the next.

The different types of credit scores

The modern credit scoring system arguably began when the FICO score was created in 1989. Today, though, there are many different types of credit scores, each one using slightly different methods to assess creditworthiness. These are some of the most commonly used:

FICO Score

The FICO Score is one of the most popular credit scoring systems, used by 90% of top lenders. It grades creditworthiness on a three-digit scale, with scores falling between 300 and 850. A higher FICO Score is better, meaning you’re more likely to be approved for credit or loan applications and benefit from lower interest rates.

It was developed in 1989 by a tech firm called Fair, Isaac, and Company (FICO) to establish an industry standard. Despite being over 35 years old, it’s still used by credit bureaus like Equifax, Experian, and TransUnion to guide billions of lending decisions each year.

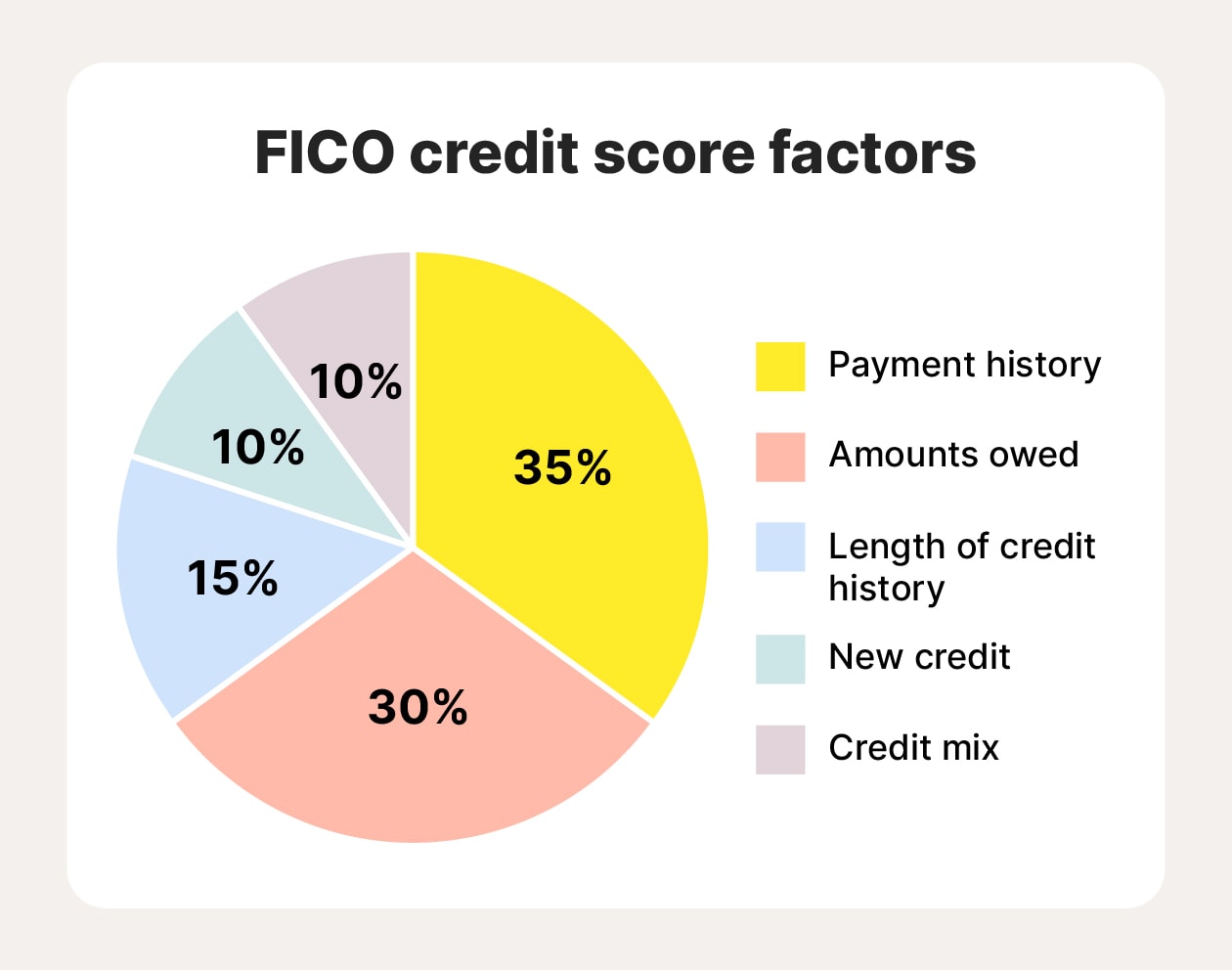

The FICO scoring model uses five factors when calculating credit scores. Here’s a summary of the factors and how they’re weighted:

Payment history (35%): Your track record of making full and timely credit card, loan, and mortgage repayments. Missed or late payments can significantly lower your score, while consistent on-time payments build it.

Amounts owed (30%): This includes your total outstanding debt and the percentage of your available credit you're using, known as your credit utilization ratio. A low (but not 0%) credit utilization ratio is generally preferable.

Length of credit history (15%): How long you’ve had credit accounts, including the age of your oldest account and the average age of all accounts. A longer credit history has a positive impact on your FICO Score.

New credit (10%): A measure of recent expansion of your total credit profile, factoring in recent credit inquiries and newly opened accounts. Multiple applications in a short time can signal risk and slightly reduce your score.

Credit mix (10%): An assessment of the diversity of your credit profile, measuring how many different “types” of credit you have. Provided your payment history is strong, a diverse mix including credit cards, mortgages, and loans contributes to a higher FICO Score.

A pie chart showing the weighting of factors that contribute to FICO scores.

What’s a good FICO credit score?

Individual lenders will interpret your FICO Score differently, but a score between 670 and 739 is deemed “Good” by FICO. A score between 740 and 799 puts you in the “Very Good” category, while a score of 800+ means your creditworthiness is considered “Exceptional.”

VantageScore

VantageScore is a credit scoring system developed in 2006 through collaboration between the three major credit bureaus: Equifax, Experian, and TransUnion. It grades creditworthiness on the same scale as the FICO model, with scores falling between 300 and 850. Within that range, VantageScore defines four “tiers” named subprime, near prime, prime, and superprime.

Just like the FICO Score model, VantageScore is widely used in the US. More than 34,000 institutions, including eight of the top ten largest banks, use it to guide their lending decisions.

The latest VantageScore model, called VantageScore 4.0, considers six factors in its credit score calculations. Here’s a summary of the factors and how they’re weighted:

Payment history (41%): An analysis of your credit payment record, with late or missed payments within the last seven years harming your overall credit score.

Depth of credit (20%): An assessment of how diverse your overall credit profile is and how long you’ve been using credit for. Generally speaking, using different types of credit over a long period will improve your credit score according to VantageScore.

Credit utilization (20%): How much credit you use as a percentage of your total credit allowance, with a particular focus on your revolving credit (e.g., credit card) accounts. VantageScore suggests that 1%–30% is an ideal credit utilization ratio.

Recent credit (11%): An assessment of the number of recent hard inquiries or new credit accounts opened. Although not a strong factor in the overall weighting, opening lots of new accounts in a short timeframe can drop your VantageScore.

Balances (6%): How much outstanding debt you have across all of your credit accounts, both current and delinquent. Typically, a lower total credit balance is better for your VantageScore.

Available credit (2%): How much credit you have available across all of your revolving credit accounts, with a higher figure generally boosting your overall VantageScore.

A pie chart showing the weighting of factors that contribute to VantageScore 4.0.

What’s a good VantageScore credit score?

It’s up to specific lenders to decide what constitutes a “good” VantageScore, depending on the type of credit application you’re making. However, scores in the prime (661-780) or superprime (781-850) range are generally seen as good.

Other credit scoring models

While the FICO Score and VantageScore are the most popular credit scoring models, they’re not the only ones. These are four other well-known credit scores used by lenders to calculate creditworthiness:

TransRisk: TransUnion’s proprietary credit scoring model, which primarily uses public records to assess creditworthiness, with scores falling on a scale from 300 to 850. TransRisk isn’t a particularly popular model due to its unconventional data sources.

Experian’s National Equivalency Score: Experian's proprietary credit scoring model ranges from 0 to 1,000, where lower scores indicate better creditworthiness. For example, a score of 100 represents a roughly 10% chance of one credit account going delinquent in the next 24 months, compared to the approximately 90% chance represented by a score of 900.

Credit Xpert Credit Score: Developed by a software company called Credit Xpert, the Credit Xpert Credit Score is based on data from the major credit bureaus. It scores creditworthiness on a scale from 300 to 850 and offers personalized recommendations for improving credit health.

CE Credit Score: A freely available and largely transparent credit score model developed by CE Analytics, scoring users on a scale from 300 to 850.

Which credit bureau is the most accurate?

No single credit bureau is the most accurate. Just like credit scores themselves, each credit bureau is slightly different, with each maintaining its own dataset based on the information it receives from lenders. Since not all lenders report to all three, your credit report can vary between bureaus.

That’s why you might see slight inconsistencies in your credit reports. Each bureau may have a different snapshot of your financial activity, depending on who reports to them and how that data is processed. Instead of focusing on which bureau is “right,” it’s smarter to monitor your credit across all three to get a fuller, more accurate picture of your credit health.

How to check your credit score and report (without hurting it)

You can access your credit report and check your credit score in several ways. Just make sure you’re using soft inquiries, not hard inquiries. Soft checks don’t affect your credit score, while hard inquiries (like those from loan applications) can temporarily lower it.

These are some of the easiest ways to check your credit score and get a credit report:

Visit AnnualCreditReport.com for a free weekly credit report from each of the three major credit bureaus.

Create accounts with the major credit bureaus to get a free credit report and credit score check directly from Equifax, Experian, and TransUnion.

Monitor your credit with LifeLock Total, with credit reports and scores from one bureau available daily and an annual report and credit score check from all three bureaus.

All of these methods are considered soft credit checks, so you don’t have to worry about your credit score decreasing when you use them to check your credit.

Help protect your credit and your identity

Worrying about which credit score is most important is less useful than working on improving your credit score. That includes protecting it from the damaging effects of fraudulent activity, like someone stealing your identity and opening new credit accounts in your name.

Beyond offering an easy way to stay on top of your credit score, with credit reports available daily from one bureau, LifeLock Total also provides credit monitoring coverage. We monitor key changes to your credit file at the three leading credit bureaus and alert you if we notice suspicious activity, so you can tackle fraud quicker and keep your credit healthier.

There is no single “actual” credit score; each credit scoring model uses slightly different criteria and formulas to create their own unique credit score. All of them are legitimate, and lenders may choose to use different credit scoring models depending on their preferences.

What credit score do lenders use?

Lenders vary in how they assess creditworthiness, and some use multiple scores in their decision-making. However, generally speaking, FICO Score and VantageScore are the two credit scores most likely to be used by lenders. FICO Score is particularly popular, used by up to 90% of top lenders in the U.S.

What is most damaging to a credit score?

The biggest threats to a credit score include late or missed payments, high credit utilization, and excessive hard inquiries. However, the exact impact depends on the scoring model, as each weighs negative factors differently.

Mark is a staff editor at Gen who specializes in cybersecurity and identity protection. He aims to help readers learn how to navigate their digital lives more safely.

Editor’s note: Our articles provide educational information. LifeLock offerings may not cover or protect against every type of crime, fraud, or threat we write about.