How to dispute credit report errors and get them removed

How to dispute credit report errors and get them removed

Errors on your credit report can drag down your score and make it harder to qualify for credit in the future. But they could also be a sign of something worse unfolding, like fraud. Learn how to dispute credit report errors. Then, get LifeLock for three-bureau credit monitoring to help catch signs of fraud and other errors if they appear again.

If you’ve spotted an error on your credit report, you have the right to dispute it. An investigation led by Consumer Reports found that nearly half of consumers who reviewed their reports spotted at least one mistake, and more than a quarter uncovered a major error that could do significant damage to their credit score.

Some of these errors, like unfamiliar accounts or hard inquiries you didn’t make, could be signs of fraud or identity theft, which can lead to serious financial consequences down the line. But, even if they’re innocent mistakes, they can impact your ability to borrow cash, obtain credit cards, get insurance, or close on that dream home.

Fortunately, there’s an established process you can follow to dispute credit report errors, get your score back on track, and improve your ability to spot errors when they appear in the future.

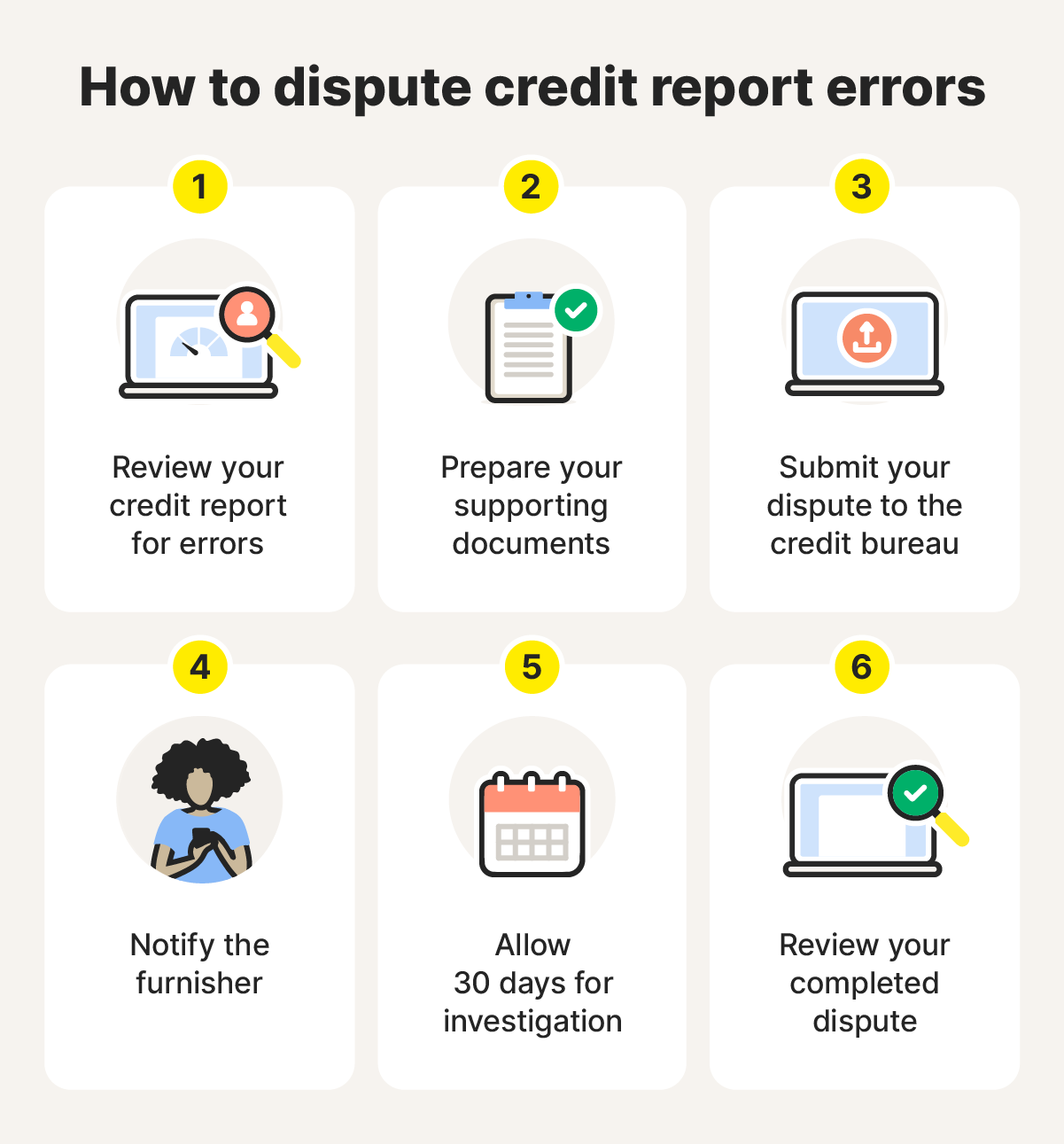

1. Review your credit report for errors

To catch errors, you’ll need to review your credit reports periodically, looking out for inaccurate or incomplete information. You can get one free credit report from each of the three major credit bureaus (Equifax®, Experian®, and TransUnion®) weekly at AnnualCreditReport.com. Alternatively, you can use a credit monitoring service to automate the process, getting alerts about potential issues when they’re detected.

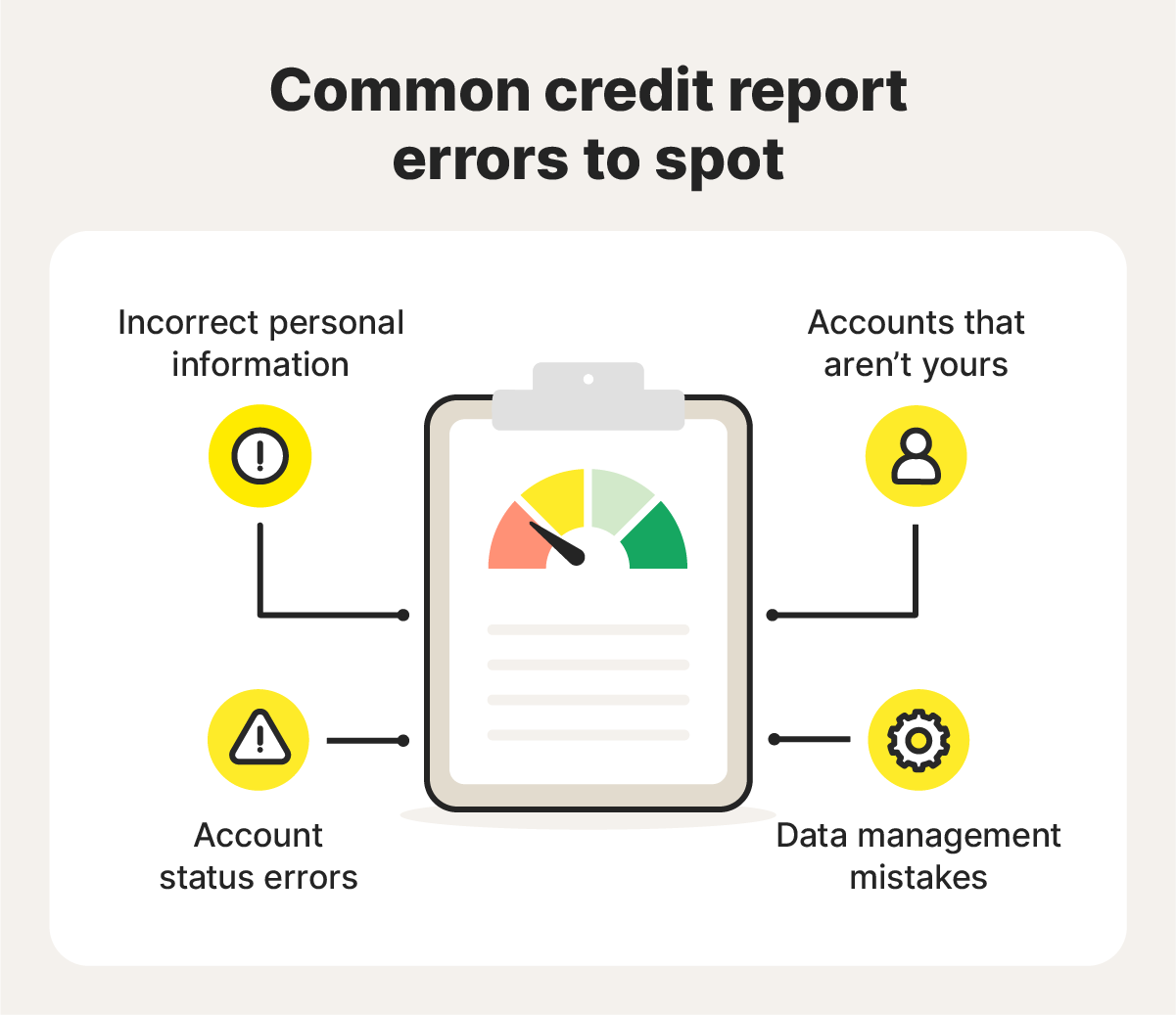

Some common credit report errors to look for include:

Incorrect personal information: The wrong name, phone number, or address, or a “mixed file” where some of your information gets confused with someone who has a similar name.

Accounts or activity you don’t recognize: Accounts you never opened or hard inquiries you didn't authorize, which are some of the most common errors that may signal fraud or identity theft.

Account status errors: Closed accounts showing as open, paid collections accounts still marked unpaid, on-time payments incorrectly marked late, or being listed as an account owner when you're only an authorized user.

Data management mistakes: Incorrect account balances, credit limits, or duplicate accounts listed under different creditors.

Incorrect public records: Bankruptcies, foreclosures, or tax liens that don't belong to you, were already discharged, or contain incorrect dates or amounts.

Outdated information: Derogatory marks, such as late payments, collections that should have been removed after seven years, or bankruptcies that still appear after ten years.

Other errors: Issues like a former joint account from an ex-spouse that should have been removed, or an account reporting the wrong type of credit (like a revolving account listed as an installment loan).

While some errors could be honest mistakes that don't affect your credit score, they're all worth investigating to rule out fraud or identity theft.

A credit report with callouts pointing to typical errors, including incorrect personal details and general data mistakes.

2. Prepare your supporting documents

Strong documentation makes it easier for investigators to verify your complaint is accurate and increases the chances of your dispute being resolved quickly. For most credit dispute submissions, you’ll want to include:

Your full name, address, and phone number.

The credit report confirmation or reference number (typically listed at the top of the report), which helps the bureau identify what specific copy you’re looking at.

A copy of the credit report where the error appears.

A clear statement explaining the error you want corrected or removed.

The account number associated with the disputed item.

You should also include copies of any additional documents that help show what actually happened. What you submit will depend on the type of error you’re disputing, but common examples include:

Proof of identity.

A utility bill.

A pay stub.

Bank statements.

Marriage or death certificates.

A letter from your lender confirming payments or account status.

Court documents.

For instance, if a closed account is incorrectly reported as open, you could attach a letter from your lender confirming the account was closed. Or, if a payment is marked late but you paid on time, include a bank statement or confirmation email that shows the actual payment date.

3. Submit your dispute to the credit bureau

You’ll need to contact the specific credit bureau whose report includes the incorrect information to alert them of the error and explain why you believe it’s a mistake. You generally have three options for contacting the credit bureaus: online, over the phone, or by sending a letter by mail.

Here’s the contact information you’ll need to dispute credit report errors with each bureau:

Equifax Information Services, LLC, P.O. Box 740256, Atlanta, GA 30374-0256

Experian, P.O. Box 4500, Allen, TX 75013

TransUnion Consumer Solutions, P.O. Box 2000, Chester, PA 19016

If you're mailing your dispute, you can use this sample dispute letter from the Consumer Financial Protection Bureau (CFPB) as a template.

[Your complete name],

[Report confirmation or reference number, if available]

[Identifying information requested by the company]:

Date of birth

Address

Telephone number

[Your return address]

[Date]

[Address of credit reporting company]

Dear [Equifax, Experian, or TransUnion],

I am writing to dispute the following information that appears on my [Equifax, Experian, or TransUnion] consumer report:

Dispute 1 [The following are meant as helpful examples; include any disputes that apply to your report].

Account number or other information to identify account: [Insert account number or other information, such as account holder names and past addresses. This is especially important if you have had multiple accounts with the same company.]

Source of dispute information: [Insert the name of the company, such as the bank, that provided the information to the credit reporting company.]

Type of disputed information: [Insert category of disputed information, such as public records information, unknown credit account/tradeline, inquiry, etc.]

Dates associated with the item being disputed: [Insert the date that appears on your report. This helps ensure that the correct account is identified by the company and identifies which aspects of the report are being disputed. You can still file a dispute if you don’t have this date.]

Explanation of item being disputed: [Insert details about why you think the information is inaccurate. Choose one of the choices below if it fits, or add your own description.]

My report includes accounts with a reported name that is different from mine.

I don’t recognize the accounts in question.

The report shows I owed money to the company that I have already repaid. [Give details about when you paid, and attach a copy of any proof that you have.]

The current status of my account is not correct. The report shows that I am delinquent, but I have made all of my payments on time. [Include account history or other information that shows the on-time payments.]

I’m the victim of identity theft, and I don’t recognize one or more of the accounts on my report. [You may wish to include a copy of the FTC report describing the identity theft.]

Other [Describe what is wrong with the report and include copies of any additional supporting documentation that you have.]

Dispute 2 [Continue numbering for each disputed item on your report and include the same information.]

[Include the following sentence if you have attached a copy of your credit report or other supporting documentation. “I have attached a copy of my report with the accounts in question circled.”]

Thank you for your assistance.

Sincerely,

[Your name]

If you suspect that the error on your credit report is due to identity theft, place a fraud alert on your credit reports, and visit IdentityTheft.gov to file a report with the Federal Trade Commission (FTC). It’s important to report identity theft ASAP to help mitigate the damage.

4. Notify the furnisher

To help resolve your dispute as quickly as possible, you should also contact the furnisher — the company that supplied the information you’re disputing to the credit bureau. This could be your bank, credit card company, utility company, or landlord.

According to the CFPB, furnishers are legally obligated to investigate credit disputes. By submitting your dispute to both the credit bureau and the furnisher, you trigger two separate investigations, which can help resolve the error faster.

Use the Federal Trade Commission's sample letter to tell the furnisher about the error you’re disputing, and include all of the same information you sent to the credit bureau, including an attached copy of the relevant credit report. You can find the furnisher's contact information on your credit report or monthly billing statement.

[Date]

[Your Name]

[Your Address]

[Your City, State, Zip Code]

[Business Name]

[Street Address]

[City, State, Zip Code]

Subject: Disputing Information in Credit Report

I am writing to dispute the following information that your company supplied to [give the name of the credit bureau whose report has incorrect information]. I have circled the items I dispute on the attached copy of my credit report(s).

This item [for instance: retailer account at ABC Department Store and the account number] is inaccurate [or incomplete] because [describe in detail what is inaccurate or incomplete and why.] I am requesting that [business name] have the item removed [or request another specific change to correct the information.]

[Add list and description of other disputed items, if that applies.]

Enclosed are copies of [my credit report and any other documents enclosed with a short description, for instance, your record of payments made] supporting my request. Please reinvestigate this matter and contact the nationwide credit bureaus to have them delete [or correct] the disputed item(s) as soon as possible.

Sincerely,

[Your name]

5. Allow the credit bureau or furnisher to investigate

Once the credit bureau receives your dispute, it has 30 days to investigate and reach a conclusion (or 45 days if you submit additional information during the investigation), and an additional five days to share its findings with you and update your report.

During this time, the credit bureau forwards your dispute to the furnisher — the company that originally reported the information. The furnisher must investigate and report their findings back to the credit bureau.

One exception: If the credit bureau or furnisher determines your dispute is frivolous or irrelevant, they can decline to investigate. This typically happens if you haven't provided enough information, or you're disputing the same item twice. If they decline, they must notify you in writing within five business days.

6. Review your completed dispute

Once the investigation is complete, the credit bureau will send you the results in writing. If they find the information is inaccurate, they'll update your credit report, and the furnisher must notify the other major credit bureaus to ensure the correction appears across all your credit files.

You can also request that the bureau notify anyone who received your report in the past six months, or in the past two years if it was for employment purposes.

Here’s an overview of the most common outcomes of a dispute you might see, and what happens next:

Outcome

What it means

What happens next

Updated

Disputed info was corrected or revised.

The updated info is reflected on your credit report.

Remains

Creditor or furnisher confirmed original information is accurate.

The disputed item stays on your report as previously listed.

Deleted

Disputed item was found to be unverifiable and removed.

The item is erased from your credit record.

7. Follow up if the dispute is not resolved

If you disagree with the results of your credit dispute and the error remains on your report, you still have options.

Reach out to the furnisher: Contact the creditor or lender directly to ask questions about your dispute result and provide documentation supporting your position.

Include a dispute statement: You can ask the credit bureaus to add a statement to your credit file describing your side of the dispute. This statement will be visible to anyone who checks your credit report.

Submit a redispute: If you've found additional documentation to support your claim, you can file another dispute. However, don't refile if you have no new evidence to provide.

File a complaint: If you believe you were treated unfairly or a valid error remains on your credit report, you can file a complaint with your state Attorney General or the FTC. Note that the Consumer Financial Protection Bureau (CFPB), which previously handled financial complaints, is currently facing operational changes.

An illustrated step-by-step guide on how to dispute credit report errors, starting with reviewing your credit report for errors.

Keep your credit report (and identity) safe

Disputing errors dragging down your credit score and having them successfully struck from the record can help you qualify for loans at better rates and terms. While the process can take time to resolve, it’s worth the effort to help you save money in the long run.

To keep a closer eye on your credit reports in the future, consider investing in an identity theft protection service that offers credit monitoring. LifeLock Total offers three-bureau monitoring that can help you catch errors across all of your reports from the major bureaus, up to $3m in reimbursement for costs following identity theft, and restoration services that can help you get back on track if your identity is compromised.

Yes, credit report disputes can work when the information you’re challenging is truly inaccurate and you include documents that support your case. Credit bureaus are required to review your dispute, and if they confirm an error, they’ll update or remove it from your report.

Do I need to dispute with all three credit bureaus separately?

It depends on where the error appears. You only need to dispute with the credit bureaus that are reporting the incorrect information. If the error shows up on all three credit reports, you'll need to file a separate dispute with each bureau.

Can disputing hurt my credit score?

Filing a dispute won't affect your credit score, but the outcome can. For example, if you dispute an inaccurate negative item that is damaging your score, and the credit bureau corrects it, your score may improve. On the other hand, if the dispute removes positive history or uncovers additional negative information, your score could drop.

How long does a credit report dispute take?

Credit report disputes typically take 30 days or less, although the investigation may extend to 45 days in some cases. The credit bureau must investigate and respond within this timeframe under federal law.

Should I hire a credit repair company or dispute myself?

You can handle credit disputes yourself for free using the steps outlined above. Credit bureaus are legally required to investigate whether the dispute comes from you or a third-party company. Credit repair companies typically charge $15-$150 per month to do the same work, so they're usually only worth considering if you're dealing with multiple complex disputes and don't have the time to manage them yourself.

Mark is a staff editor at Gen who specializes in cybersecurity and identity protection. He aims to help readers learn how to navigate their digital lives more safely.

Editors' note: Our articles provide educational information about identity theft, scams, financial fraud, and other topics that can put your identity or personal accounts at risk. LifeLock offerings may not cover or protect against every type of crime, fraud, scam, or threat we write about. For more details about how we write, review, and update our articles, see our Editorial Policy.